North-Central China Offers Massive Market Opportunity for Mongolian Coal Miners

Mongolia's massive and low-cost coal reserves are well-positioned to serve seven nearby Chinese provinces with more than one billion tonnes of annual coal demand

August 21 (China SignPost) On 7 June 2012, Mongolian Mining Corporation (MMC) broke ground on a rail line that will link its Ukhaa Khudag (UHG) coking coal mine to the Chinese border crossing atGashuun Sukhait (GS) and help move coal far more cheaply than the 400 trucks currently doing the job. MMC recognizes that China, which took 99% of Mongolia's coking coal exports in 2011, is Mongolia's best option for multi-million tonne per year thermal and coking coal exports. Low coal production costs can make Mongolian coal highly competitive in seven nearby Chinese provinces that consumed more than a billion tonnes of coal in 2010, according to official data.

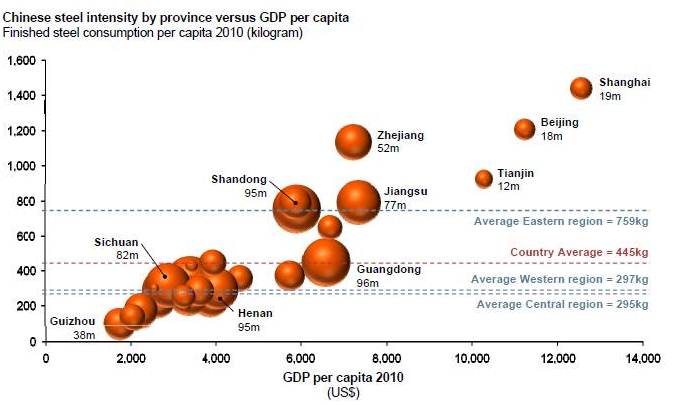

The per capita steel demand levels in the populous and fast-growing provinces of Central and Western China are still only 40% of the levels seen on China's East Coast (Exhibit 1). As the Chinese economy recovers, these regions—which are the most accessible to Mongolia's landlocked coal producers—will provide growth markets able to absorb rising Mongolian coal exports.

Exhibit 1: Chinese steel intensity by province versus GDP per capita

Finished steel consumption per capita, kg (2010)

Source: DRC Report, NBS, BHP Billiton

Note: select provinces and regions show population (e.g., "Shanghai 19m" = 19 million population)

Mongolian coal projects should expect to operate on Chinese regional coal prices, which will likely rise closer to global seaborne prices as the Chinese government consolidates the mining sector and caps domestic coal production by 2015 and China's proportion of seaborne thermal coal supply rises. Investors should also look beyond rail routes through Russia and consider alternative ways of monetizing coal reserves such as mine mouth power plants that use ultrahigh voltage power lines to move electricity to markets in China and Russia as well as coal-to-liquids (CTL) and coal-to-chemicals (CTC) plants. These approaches can capitalize on growing coal demand in Western and Central China and can improve Mongolian coal miners' pricing power by putting Chinese coal traders on notice that the coal they want could alternatively be sold as electrons, motor fuel, or petrochemicals.

Exporting coal through Russia is cost prohibitive and rising Russian exports to Asia already strain Russia's rails and Pacific ports. A 90 million tonnes per year (tpy) decline in European and Russian coal demand since 2000 has re-oriented coal producers toward the Asian market. Russian miners increased coal exports to coal-hungry China from only 42 thousand tonnes in 2001 to 10.5 million tonnes in 2011 and are aiming for 15 million tpy by 2015.

With European coal demand in a death spiral, politically-savvy Russian coal exporters like SUEK and Mechel will fight hard, and most likely successfully, to keep Mongolian coal off Russian rail lines and out of their Pacific Coast terminals. Russian Railways plans to substantially increase east-bound coal hauling capacity by 2020. However, with seven major coal projects in Siberia and the Russian Far East aiming to bring as much as 80 million tpy of productive capacity online by 2020 and export terminal capacity likely to grow by less than 30 million tpy, severe capacity constraints will remain and Mongolian coal will be left out in the Siberian cold.

So where does the lack of a high-volume Russian rail route leave companies planning to develop coal projects in Mongolia? One strategy is to accept Chinese regional prices, become low-cost suppliers in North-Central China, and go for volume. Mongolian surface miners in the Southern Gobi with a rail line can deliver coal 500 km into China at cost of insurance and freight (CIF) of less than US$60 per metric tonne (mt), less than the CIF of local Chinese underground miners, which can exceed US$70/mt to the same destinations. Mongolian mines will face competition from new low-cost thermal coal supplies from Xinjiang, but the two sources have similar mining costs and Mongolian miners will have shorter shipping distances to the North-Central Chinese market.

Mongolia's coal export focus on China will have major risk implications in both coal and natural gas markets, as well as oil markets if investors also build China-facing CTL and CTC projects.Mongolia's low cost and geographically captive thermal and metallurgical coal supplies will likely help undermine Beijing's plans to reduce China's dependency on coal and, in conjunction with new coalfields in Western China's Xinjiang Province, could even jeopardize PetroChina and Sinopec's ambitions to develop shale gas and other unconventional resources.

The Chinese seek secure, well-priced mineral supplies from their neighbor, not a re-enactment of the Qing Dynasty period of political domination. Russian transport infrastructure constraints, Russian companies' antipathy toward competition from Mongolian coal, and the tyranny of distance will naturally direct mineral flows to China. To realize great economic opportunities in an otherwise somewhat sputtering China market in 2012, Mongolia must establish political and regulatory stability and recognize that China needs—and can absorb—large volumes of Mongolian coal exports. Meanwhile, to facilitate this development and profit in the process, investors in Mongolian coal should build rails south, run mines at full bore, and also consider opportunities in the coal-by-wire, coal-to-liquids, and coal-to-chemicals sectors.

August 21 (China SignPost) On 7 June 2012, Mongolian Mining Corporation (MMC) broke ground on a rail line that will link its Ukhaa Khudag (UHG) coking coal mine to the Chinese border crossing atGashuun Sukhait (GS) and help move coal far more cheaply than the 400 trucks currently doing the job. MMC recognizes that China, which took 99% of Mongolia's coking coal exports in 2011, is Mongolia's best option for multi-million tonne per year thermal and coking coal exports. Low coal production costs can make Mongolian coal highly competitive in seven nearby Chinese provinces that consumed more than a billion tonnes of coal in 2010, according to official data.

The per capita steel demand levels in the populous and fast-growing provinces of Central and Western China are still only 40% of the levels seen on China's East Coast (Exhibit 1). As the Chinese economy recovers, these regions—which are the most accessible to Mongolia's landlocked coal producers—will provide growth markets able to absorb rising Mongolian coal exports.

Exhibit 1: Chinese steel intensity by province versus GDP per capita

Finished steel consumption per capita, kg (2010)

{kind=link}

Source: DRC Report, NBS, BHP Billiton

Note: select provinces and regions show population (e.g., "Shanghai 19m" = 19 million population)

Mongolian coal projects should expect to operate on Chinese regional coal prices, which will likely rise closer to global seaborne prices as the Chinese government consolidates the mining sector and caps domestic coal production by 2015 and China's proportion of seaborne thermal coal supply rises. Investors should also look beyond rail routes through Russia and consider alternative ways of monetizing coal reserves such as mine mouth power plants that use ultrahigh voltage power lines to move electricity to markets in China and Russia as well as coal-to-liquids (CTL) and coal-to-chemicals (CTC) plants. These approaches can capitalize on growing coal demand in Western and Central China and can improve Mongolian coal miners' pricing power by putting Chinese coal traders on notice that the coal they want could alternatively be sold as electrons, motor fuel, or petrochemicals.

Exporting coal through Russia is cost prohibitive and rising Russian exports to Asia already strain Russia's rails and Pacific ports. A 90 million tonnes per year (tpy) decline in European and Russian coal demand since 2000 has re-oriented coal producers toward the Asian market. Russian miners increased coal exports to coal-hungry China from only 42 thousand tonnes in 2001 to 10.5 million tonnes in 2011 and are aiming for 15 million tpy by 2015.

With European coal demand in a death spiral, politically-savvy Russian coal exporters like SUEK and Mechel will fight hard, and most likely successfully, to keep Mongolian coal off Russian rail lines and out of their Pacific Coast terminals. Russian Railways plans to substantially increase east-bound coal hauling capacity by 2020. However, with seven major coal projects in Siberia and the Russian Far East aiming to bring as much as 80 million tpy of productive capacity online by 2020 and export terminal capacity likely to grow by less than 30 million tpy, severe capacity constraints will remain and Mongolian coal will be left out in the Siberian cold.

So where does the lack of a high-volume Russian rail route leave companies planning to develop coal projects in Mongolia? One strategy is to accept Chinese regional prices, become low-cost suppliers in North-Central China, and go for volume. Mongolian surface miners in the Southern Gobi with a rail line can deliver coal 500 km into China at cost of insurance and freight (CIF) of less than US$60 per metric tonne (mt), less than the CIF of local Chinese underground miners, which can exceed US$70/mt to the same destinations. Mongolian mines will face competition from new low-cost thermal coal supplies from Xinjiang, but the two sources have similar mining costs and Mongolian miners will have shorter shipping distances to the North-Central Chinese market.

Mongolia's coal export focus on China will have major risk implications in both coal and natural gas markets, as well as oil markets if investors also build China-facing CTL and CTC projects.Mongolia's low cost and geographically captive thermal and metallurgical coal supplies will likely help undermine Beijing's plans to reduce China's dependency on coal and, in conjunction with new coalfields in Western China's Xinjiang Province, could even jeopardize PetroChina and Sinopec's ambitions to develop shale gas and other unconventional resources.

The Chinese seek secure, well-priced mineral supplies from their neighbor, not a re-enactment of the Qing Dynasty period of political domination. Russian transport infrastructure constraints, Russian companies' antipathy toward competition from Mongolian coal, and the tyranny of distance will naturally direct mineral flows to China. To realize great economic opportunities in an otherwise somewhat sputtering China market in 2012, Mongolia must establish political and regulatory stability and recognize that China needs—and can absorb—large volumes of Mongolian coal exports. Meanwhile, to facilitate this development and profit in the process, investors in Mongolian coal should build rails south, run mines at full bore, and also consider opportunities in the coal-by-wire, coal-to-liquids, and coal-to-chemicals sectors.

Comments

Post a Comment